- GTG Weekly

- Posts

- 💸 Fed Pauses. Rates Don’t.

💸 Fed Pauses. Rates Don’t.

Mortgage Rates Up (again) ⬆️. Sedona trip. Fed pause. Helocs looking hot. Oil pushing inflation which pushes bonds... which pushes rates.

Glenn Groves

March 24, 2026

Sponsored by

Issue 149 - Hello and Happy Tuesday.

Markets are still working through a mix of inflation concerns, global tensions, and uncertainty about where the economy heads next. That uncertainty has been keeping pressure on the bond market, which is why mortgage rates are still hovering at elevated levels.

Even though the Fed chose to hold steady again, long-term fixed rates are continuing to react more to market volatility and inflation expectations than to any single Fed decision. When investors are unsure about the outlook, rates tend to stay higher until there is clearer direction.

One interesting dynamic right now is that not all loan options are being impacted the same way. While fixed-rate pricing has been moving around with the bond market, some prime-based products like HELOCs have remained more stable, which is a little ironic considering they technically adjust monthly, yet lately they have been the calmer option in the room. And yes, we offer these, so PLEASE ASK!! |  Giphy |

We break that down further below, but for now the key theme is simple: uncertainty is keeping rates elevated, and that is creating some unexpected strategy opportunities.

Personal Note:

The family took a trip last week to Sedona, AZ, for Spring Break, hence why there was no newsletter last week. Had a great time together, of course, the main attraction for the kids was the hotel pool and hot tub, lol.

Jamie is going after some sunset pics.

Visited the National Monument, Montezuma’s Castle. |  Zoom in, and you can see Jamie and JJ! |

TLDR (Too Long Didn’t Read) Summary

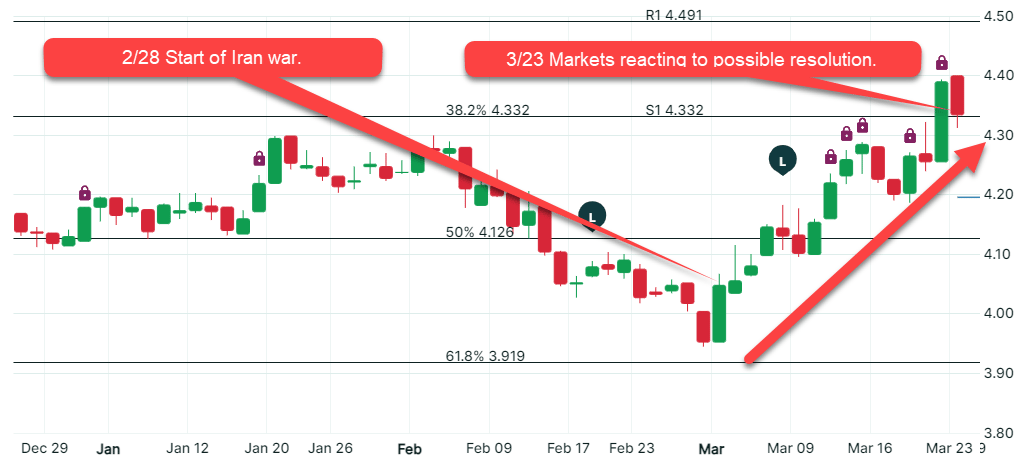

⬆️ RATES - All sectors move up on continued uncertainty in the Middle East.

📊 TECHNICALS - Fed PAUSE. Puts HELOCs on a pedestal.

Experts Would Invest $100,000 in This Alternative Now

A new Knight Frank report made an unexpected declaration. It revealed that 44% of family offices are investing more in residential real estate now. And, you don’t need to be Warren Buffet to see why.

Since 2000, residential real estate outperformed the S&P 500 by 70% in total returns. It’s the only asset that pays you to own it, grows while you sleep, and shields your gains from the IRS.

That’s why you need mogul. It’s a real estate platform that lets you invest in institutional-grade rental properties. You get monthly rental income, capital appreciation and tax benefits without a down payment or 3 a.m. tenant calls. In fact, over 20,000 investors have joined.

Here’s Why:

• Tax Benefits

• +7% annual yields

• 18.8% avg annual IRR

TLDR: You can invest in high quality real estate for a fraction of the cost. Why wait?

Past performance isn't predictive; illustrative only. Investing risks principal; no securities offer. See important Disclaimers

INTEREST RATES

Rates 📢 March 24th, 2026

10 Year T-Note 180-day snapshot

Product | Rate / APR | Weekly Change |

|---|---|---|

⬆️ Conv. | 6.490% / 6.521% | +.375% |

⬆️ Conv. HB | 6.625% / 6.650% | +.125% |

⬆️ JUMBO | 6.500% / 6.523% | +.375% |

⬆️ FHA 3.5% DP | 5.750% / 6.693% | +.250% |

⬆️ VA 0% DP | 6.000% / 6.232% | +.375% |

Rate data as of morning of publication. Unless noted otherwise, all scenarios are assuming 30 Year-Fixed mortgage, Purchase or R/T Refinance. No origination points charged, 780 FICO score, and 20% down payment. Provided for consumer education only and does not serve as a binding offer to extend lending. Payment period, interest rate, APR, and other terms subject to income, asset, and credit profile qualification. Provided courtesy of GTG Financial, Inc. NMLS 1595076. Equal housing opportunity. www.nmlsconsumeraccess.org

⏱️ Rates in 60 Seconds

📉 Markets like the headlines… lenders not convinced yet

Stocks are rallying on optimism that tensions with Iran could ease, but mortgage pricing has not followed yet. Lenders are waiting to see if this sticks before improving rates.

📊 Bonds still cautious

Mortgage bonds are hovering near key technical levels. They’ve improved slightly, but not enough for meaningful rate relief yet.

🛢️ Oil moving lower helps the story

Lower oil typically helps the inflation outlook, which is good for bonds and mortgage rates in the longer term. But markets want confirmation, not just headlines.

🏦 Why rates remain elevated

Lenders price conservatively when volatility is high. With conflicting headlines about negotiations, they are holding margins wider until direction becomes clearer.

👀 What Realtors should watch this week

Tuesday: ADP Employment Report

Wednesday: Mortgage Applications

Thursday: Jobless Claims

Strong labor data could push rates higher again. Softer data could help bonds recover.

Realtor Insight 💡

Even though the news cycle sounds positive, mortgage pricing has not caught up yet. Buyers waiting for an immediate drop may need patience. If tensions truly ease and inflation expectations improve, we could see pricing improve in the coming weeks, but lenders want confirmation first.

For now, we remain in an elevated but potentially improving range.

TECHNICALS

Fed Pauses Again. Why HELOCs Just Got More Competitive

🏦 The Fed paused again

The Federal Reserve kept the Fed Funds Rate unchanged at 3.50% to 3.75% for the second straight meeting. The Fed is still waiting for clearer direction on inflation, jobs, and global risks before making its next move.

📈 But long-term fixed rates are still moving

Mortgage rates are driven more by the bond market than the Fed directly. Recently, volatility tied to inflation concerns and global conflict has pushed long-term fixed rates higher, even while the Fed stands still.

🔄 Rare shift in loan product competitiveness

Prime-based products like HELOCs are tied to the Prime Rate (currently 6.75%), which typically only moves when the Fed changes policy. Because the Fed paused, prime has remained relatively stable, while fixed-rate pricing has been pushed around by bond market swings. Obviously, individual scenarios will add or subtract from the prime pricing for specific HELOCs.

Giphy

💡 Why this matters right now

This is one of those rare moments where fixed-rate loans are adjusting quickly, but HELOCs and some ARMs are not moving as much, making them more competitive than usual. When fixed rates rise quickly, prime-based financing can suddenly look like a very efficient option for borrowers with strong equity positions.

⚠️ Important context

HELOCs are still variable-rate loans, so future Fed moves can impact pricing. But in the current environment, prime-based financing is not experiencing the same volatility as long-term fixed rates.

Realtor Insight

🏡 When clients have meaningful equity, it may be worth exploring HELOCs, ARMs, or hybrid structures instead of assuming the 30-year fixed is automatically the best execution in today’s market.

Reply